Cheat Sheets Premium: Finding the Best Dividend Paying ETFs

96 ETFs Following a Dividend Paying Strategy Are Squared Off to Help You Find the Best Combination of Value, Strength, Timing & Yield

Many retirement-aged investors lean on dividends (and social security) to make their personal household balance sheet square up. The idea is to receive a stream of income that just keeps coming no matter how stock prices fluctuate. Some dividend investors never actually touch their nest egg as prices move up and down through stock bull and bear markets.

So, since we’re living through maybe our fourth bear market rally of the year, and sadly unlikely to be the last of this cycle, it’s a good time to get a sense of whether dividend investing through bear markets actually pays off.

To save space for our premium stack ranking exercise today — which will be all about managing a dividend portfolio with the potential to grow capital over time while maximizing yield, we’ll use this audio embed below to share some of my analysis of market returns over the past century - plus. This will help dispel the myth that dividend strategies come any where near the risks of “buy low and sell high” stock investing that retired investors relying on the “Four Percent” rule face, when attempting to draw down their portfolios for investment income That’s where you figure out how and when to sell 1/25 of your life savings to pay for a year of your retirement. Aggggh! The pressure!

In this audio embed, I’ll also share my own retirement income strategy (but I won’t give retirement advice , because I’m neither licensed nor qualified for that). I’m practicing, just like you, validating my trading plans through simulated and some live trading. accounts. It’s really important to know what you’re getting into, because in retirement you gotta make it work.

In the years I have left before I have to trade without a W2 parachute, I plan to practice until it’s boring to make my monthly “nut”. So what’s my 3-pronged retirement income strategy to pay bills, take vacations and do old-people stuff? And how does this long winded babble serve as Cheat Sheet’s Premium Service you pay $5 bucks of your hard earned cash for. We’ll cover all that in less than eight minutes. No, don’t cancel. I need the retirement money. Plus, I promise the plan I’m about to share with you related to dividend investing (even though we’re only scratching the surface) is one you’ll find valuable, and perhaps even view it skeptically as too good to be true. Although I’m polishing the story for maximum effect, I promise I’m not bull-shitting. I

Audio Embed Summary

The dividend growth rate is far less volatile that stock market returns, with few exceptions. Dividend strategies hold up in bear markets.

Cheat Sheets provides objective data to help you rebalance a dividend portfolio based on relative strength quarterly, monthly or semi annually. By focusing on ETFs or stocks featuring companies with a history of raising their dividends decade in and decade out, or by using trading signals to effectively anticipate companies entering the those ranks, we’ll be able to make a calm transition out of W2-land.

My personal retirement strategy includes:

Starting social security at age 62. A controversial decision.

Using options to generate passive income off my stock and ETF holdings. This will continue to be a big part of Cheat Sheets content because it is THE untapped opportunity for Americans who saved.

Actively managing my holdings for present dividend strength, using Cheat Sheets market data - relative strength rank and trend reports in particular — for selection purposes, and market forecast triggers for timing purposes.

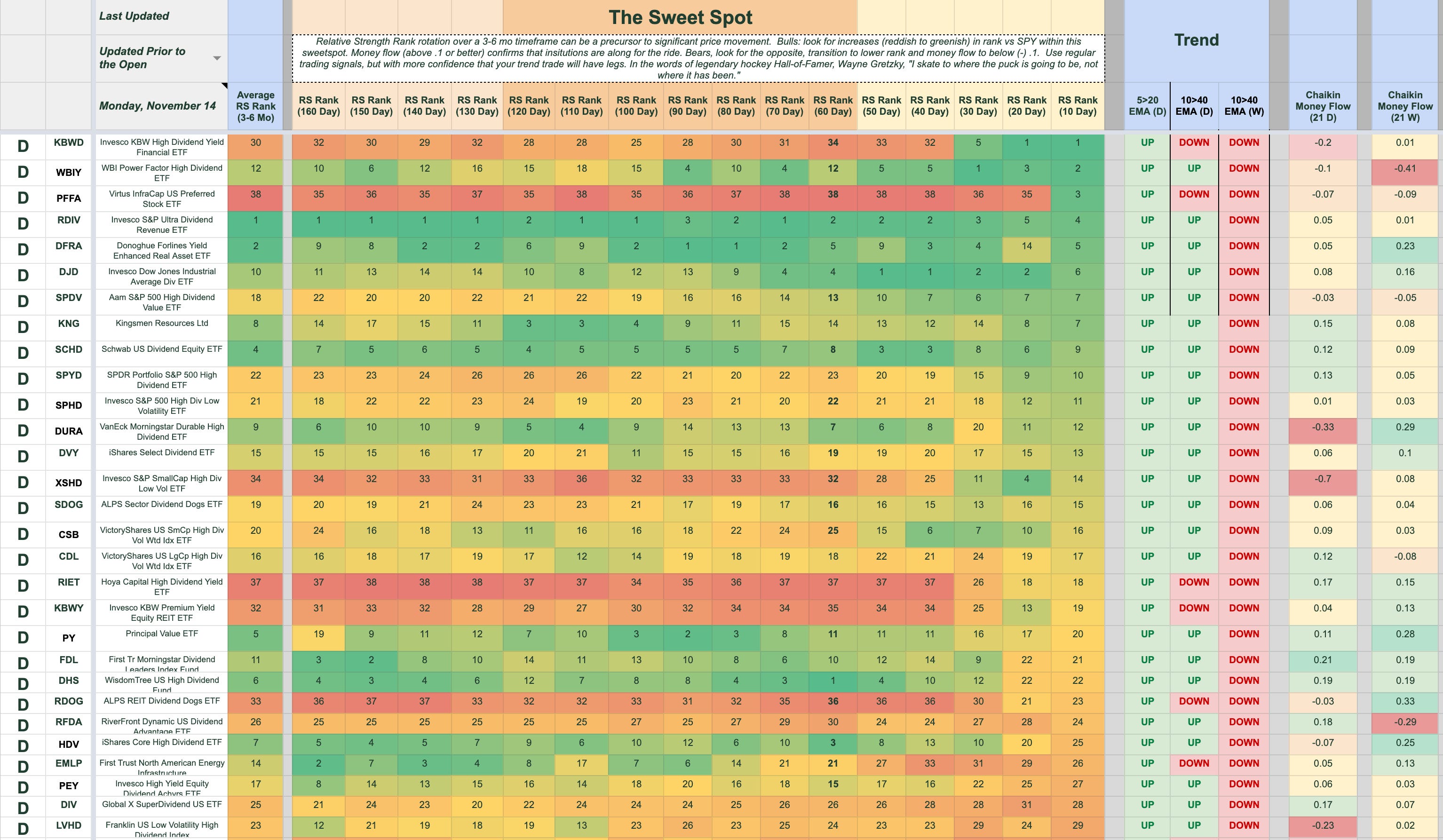

Cheat Sheets Premium Rank and Trend Reports for the Dividend Strategy ETFs

We started with a list of 96 ETF’s dedicated to Dividend Investing as their core strategy. We allowed all types of Dividend Investing to be included in our initial screem from sector/industry specific to market cap weighted to global/regional/emerging market strategies, and even actively managed and passively indexed ETFs

For this first pass, we also let the fund manager get away with her or his bullshit fees (in excess of .5% of assets under management we call bs!). Let’s see if these bozos deserve it. Note to self: be sure to strip out ETFs with annual expenses above .5% from any final list, and focus on those ETF’s with management fees in the .1% to .2% range….as in “point 1 percent, just so we’re clear”.

The jury came back long ago about in the form of studies, and how much they drain lifetime savings from the average investor. It’s like death by a thousand paper cuts.

Tnen, we applied our initial filter

$10 per share minimum

1,000,000 shares traded on average daily. This is a aggressive and will eliminate boutique ETFs that may have solid management. For me, liquidity matters in markets that are going to be near the brink of meltdown for quite a while, maybe the rest of my life.

To be valid for our “Here and Now” strategy of turning over holdings inside retirement accounts (to avoid tax consequences) that allows for quarter ly rebalancing, we required a current yield of 3%. Some strategies involve out of favor stocks or other financial instruments. Others are not actively managed. Still others are, but the ETF advisor is incompetent and asleep at the wheel. The liquidity filter, by requiring high volume eliminates a lot of that riff raff.

Here are the 40ish ETFs Yielding 3% or More Following a Dividend Specific Optimization Strategy.